By this we mean should you reduce your equity exposure within your pension?

Our attitude to risk naturally changes as we get older. When we are in the wealth accumulation phase in our twenties and thirties we are more likely to have a higher risk portfolio as we have many years till retirement. This might change slightly as we move in to our forties and again as we progress into our fifties.

The advice from most pension providers and advisors is to change the allocation to your pension approximately 5 years prior to your retirement/drawdown date. This is to reduce the risk within your portfolio and to ensure you can sustain your requirement income and are not affected by significant deviations in the market. However, is still correct and best advice?

Reducing your risk exposure would normally mean changing your allocation to approximately 20-40% equities and the remainder to fixed income, property and cash etc. The logic behind this advice makes a lot of sense. However, reducing your equity exposure inevitably will reduce your annual returns and when drawing upon your pension surely you still require a healthy return to sustain your annual drawdown?

What does a cautious allocation look like?

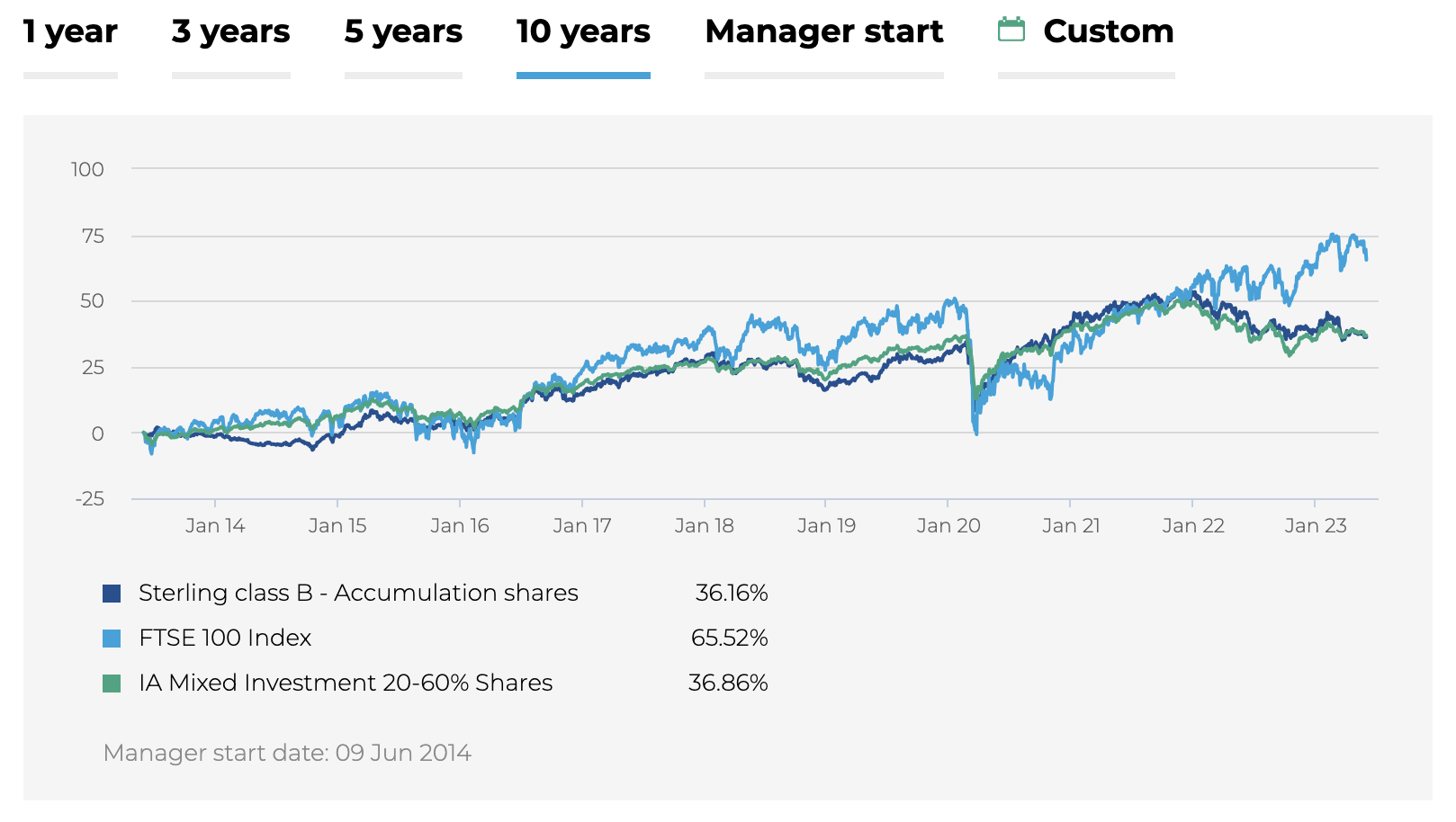

As discussed earlier if we reduce our equity exposure we reduce our future potential returns. For illustration purposes only we have chosen the Premier Miton Cautious Multi Asset Fund.

This fund has a cautious allocation of 50% equities, 40% fixed income, 7% commodities and 2% in cash. Below you can see the previous 10 years returns against their chosen benchmark.

Here are some examples

If an individual of 40 years of age invested and initial amount of £100,000 in an S&P 500 ETF and a further £1,000 per month until 65. They would have accumulated a pension fund of £2,500,000 given the average return of the S&P 500 over the past 20 years has been 10.05%. In addition, they would have benefited from compound interest and unit cost averaging which would help mitigate risk and smooth out returns.

If they selected a low risk approach like the fund above, rather than have 2,500,000 their pension fund would be valued at just 670,000. This illustrates the significance and impact of a higher equity exposure over time.

When you reach retirement the idea is to live off the interest in order to ensure you do not deplete your funds and can sustain an income for as long as you live. According to the Federal Statistical Office the life expectancy in Switzerland is one of the highest in the world with men born in 2021 living till 81 years of age and women living until 85. This is only a guide and many of us will live well into our 90’s if not reach the 100 milestone. With this in mind in order to ensure we have enough capital to last a further 20+ years from retirement and also allow us to leave our legacy behind to our beneficiaries it can prove a difficult challenge.

Potential Income

Given the above two examples of investment, if the cautious investor lived off the interest alone their annual income would be 21,000. The more aggressive investor would be able to draw an income of 262,500.

OK so you can potentially benefit from a larger pension fund but should you remain invested in the high risk portfolio when you retire?

Pensions are a lifetime investment

When investing in higher risk portfolios, it is always important to ensure you have time on your side. Warren Buffet once said “it is time in the market and not timing the market”. If you are saving for a property purchase and are likely to require the funds within the next 3-5 years then a cautious allocation would be more beneficial as you would have very little time for your portfolio to recover from a period of negative performance.

Your pension fund is likely to be with you your entire lifetime and as explored above this could be anywhere between 20-30 years after retirement. With this in mind, time is also on your side in retirement even though you will be drawing an income.

If your portfolio generates higher returns you can withdraw this amount as income (262,500), whilst preserving your pension capital. If you only require 100,000 income to live on your pension fund would continue to grow, even though you are in drawdown. This is a very tax efficient way of leaving capital to your loved ones as pension funds do not form part of your estate.