Unfortunately it was inevitable that the BOE would start to increase interest rates in order to help combat rising inflation. However, did you know that this could have a serious impact on the open market value of your defined benefit pension benefits?

In order to understand why interest rates have an effect on final salary CETV’s, we need to understand how your scheme actuaries calculate your CETV (cash equivalent transfer value).

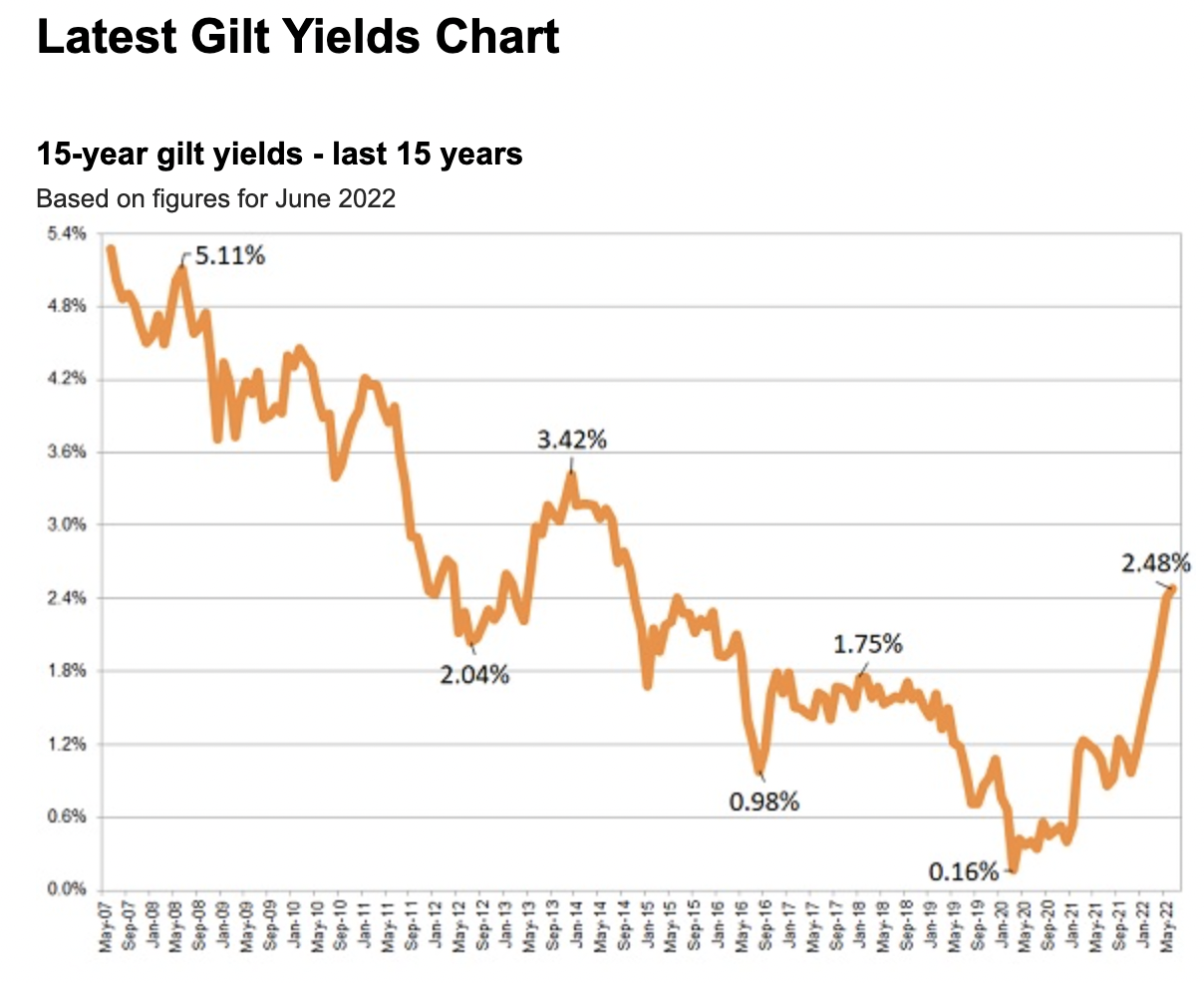

Why have we seen record high CETV’s over the past few years?

We have seen CETV’s reach record values in the past years. In some instances our clients have received offers of over 30 x their promised annual income (Prior to COVID-19 our clients valuations were closer to 20 x). At the very start of the COVID-19 pandemic the BOE reduced interest rates even further to help boost the UK economy. As a result we saw interest rates cut to just 0.1% and the UK 10 year gilt rate at 0.237%.

Final Salary Pension transfer values are closely linked to the value of UK gilt rates and when we see them decrease in value we see a rise in CETV valuations. The same is true in reverse and as we see gilt rates rise alongside interest rates, transfer values (or CETV’s) often reduce.

How are CETV’s calculated?

When your pension scheme calculates your CETV, this is based on many variables and factors. These include;

- Your age

- Potential life expectancy

- Cost of living

- Your marital status

- Your schemes NRD – Normal retirement date

- Current gilt rates

In addition defined benefit pension schemes represent a heavy burden of liability on companies balance sheets and the desire to reduce and eventually eradicate this fluctuating liability can result in companies artificially inflating CETV’s further to encourage members to move to private pension arrangements.

Why are UK Gilt yields important?

Gilt rates have long been used by the actuaries that calculate the ongoing requirements of a defined benefit scheme to meet it’s member’s promised pension benefits. They form a major part of how much this provision will cost the scheme.

When gilt rates are higher, the assumed cost of providing members pensions is therefore lower, leading to potentially lower CETV’s. In recent years and still at today’s rate, this has resulted in strong CETV’s being offered to members to transfer their benefits away from the scheme and into their own private arrangements.

Are they likely to reduce in value?

Although we do not have a crystal ball, what we can do is look back at what we have learnt from the previous years. It is clear that a higher interest rate environment could pave the way for lower CETV values. If you currently have a final salary pension, it would be worth while requesting an up to date CETV.

Additional benefits to potentially opting out of your Final Salary Pension

There are many potential benefits to opting out of your existing scheme but you must seek professional advice in order to establish which ones may apply to your current circumstances. These include;

- Secure your high transfer value

- Ensure 100% of your pension is left to your chosen beneficiaries (Wife and Children)

- Consolidate your final salary pension with your other personal and company pensions

- Generate a higher income drawdown

- Reduce your tax liabilities

- Select a currency that is relevant to you. (EUR, CHF, USD) Prevents exposure to future foreign exchange fluctuations

- Crystallise your Final Salary pension at its current value. Pay no additional taxes on the growth

ACT NOW! and review your UK Final Salary Pension

More information about transfer values can be found at the UK’s pension regulator website