With the recent reduction in CETV’s, Should you still consider transferring?

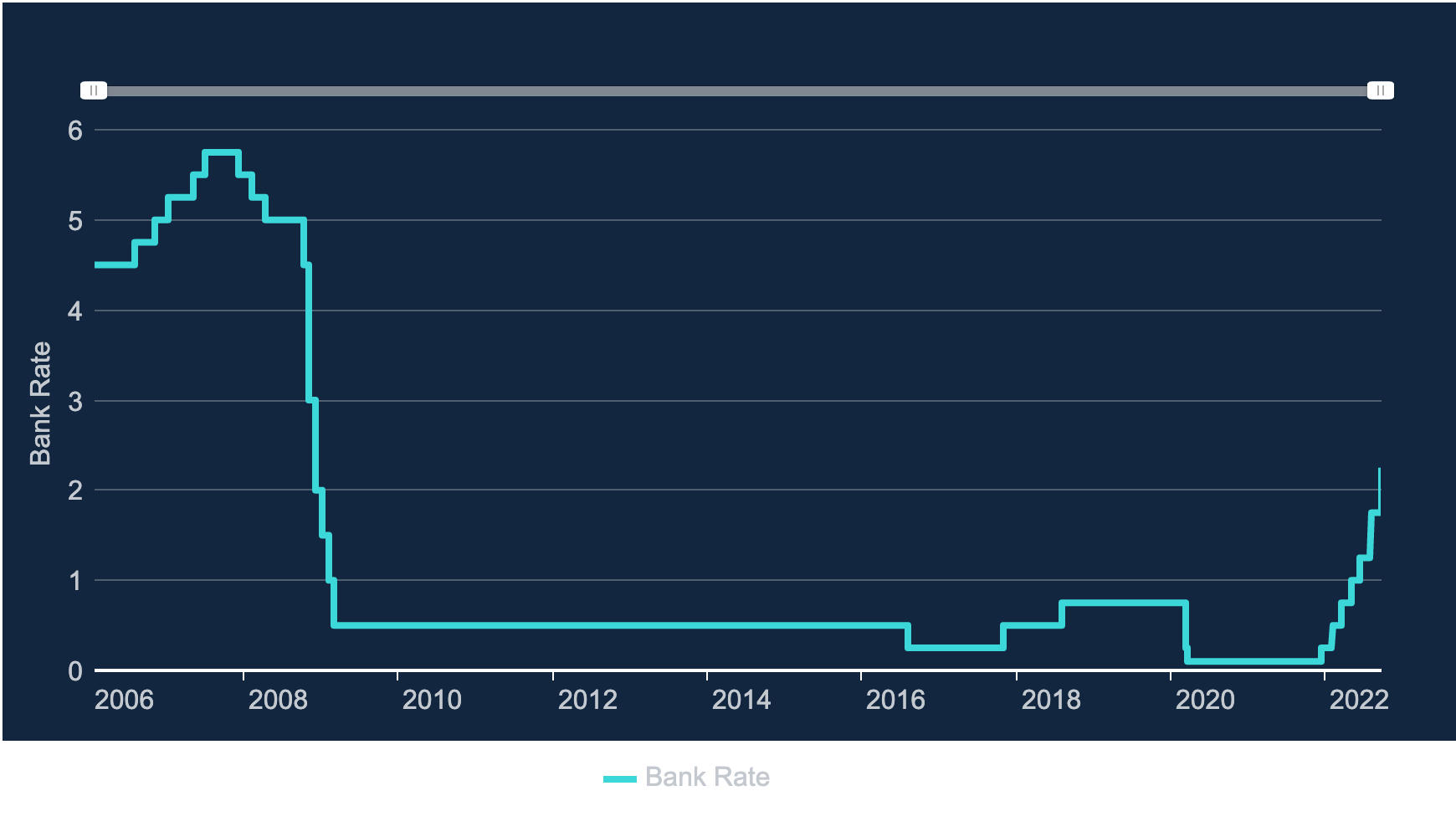

As we predicted and have written articles about before. The new higher interest rate environment has caused CETV’s to fall and in some cases the difference is significant. So you should not transfer and wait for the values to recover right? Wrong! It is extremely unlikely that we will see interest rates back below 1% and even if the BOE are successful in bringing the rates of inflation under control, they will not revert back to the low rates we have all become accustomed since 2009.

Realistically we are likely to see rates settle between 1.5% – 2% and given the current BOE interest rate is now 2.25%, current CETV’s are probably what we should expect for future transfers. However, in the short term rates are likely to rise further which will force valuations even lower.

So the question is should you consider opting out of your Final Salary pension?

The answer to this question will depend on the individual and their personal circumstances and you should always seek professional financial advice before making your decision. Your advisor will discuss your future requirements and retirement goals in order to make their recommendations. But here are some tips.

Do not get hung up on your pension transfer value.

Even if your valuation has fallen in the past 6 months, it could still be beneficial to opt out as it may still be possible to increase your income post retirement and also maximise the pension available to your spouse or children.

The industry average for most CETV’s is 20 X your promised income, so anything offered above this rate is a bonus.

Here is an example using a transfer value of 20 X.

If your promised income is £20,000 per annum and your spouses pension is £10,000 (upon death). You could be offered £400,000 should you opt out. So are there benefits of potentially taking advantage of this offer?

This will likely depend on how many years away from retirement you are. If a 40 year old received this offer and their NRD was 65, they could potentially invest this capital for 25 years. If they received a modest return of just 5% per annum their pension fund would then be worth just under £1,400,000.

So how much income would this provide?

If you do not buy an annuity, the general idea is that you drawdown your pension at the rate of growth you achieve. This ensures you are able to provide a pension for as long as you live and do not deplete the fund. So in this example, a drawdown of 5% would generate an income of £70,000 per annum and more importantly upon your death your spouse/children will receive 100% of the remaining pension fund and also be able to drawdown £70,000 per annum. This is instead of receiving 50% of the promised income (£10,000).

Is the life time allowance applicable?

The £400,000 CETV is well under the current LTA of £1.,073.100, so no additional taxes would be due.

So if your pension has grown to £1,400,000 would the LTA be applicable? This would depend on the structure of your pension. If you transferred your pension into a SIPP, then yes the LTA tax charge would be triggered. However, if you transferred your pension into a QROPS, at the time of transfer you would trigger a Benefit Crystallisation Event (BCE), which will freeze your pension at this level for tax purposes. So in this example no additional LTA taxes would be applied to your pension.

As you can see from the above example it can be extremely advantageous to opt out in some circumstances. If you wish to review your Final Salary Pension, our trained team at SuisseRock will be delighted to help you.

How To Review Your Pensions

You can schedule your complimentary review by simply completing the form below. Once submitted our team will contact you and start the review process.