If so, you could be liable for an additional 55% tax

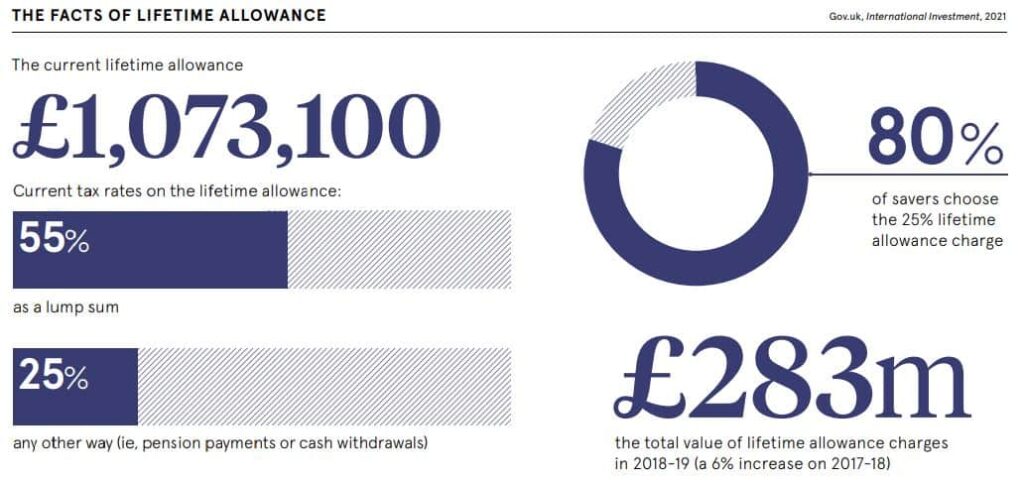

If your pension fund already or will exceed the UK life time allowance before you crystallise your benefits, you are potentially going to be liable to pay the additional 55% tax when they draw upon your UK pension assets. This is mainly due to the Lifetime Allowance (LTA) being reduced significantly over the past years. For example between 2010 and 2012 the LTA was £1,800.000 and now it is just £1,073.100.

So what is the Lifetime Allowance?

The Lifetime Allowance or LTA is a limit on the amount of pension benefit that can be drawn from pension schemes – whether lump sums or retirement income – and can be paid without triggering an extra tax charge.

What does this mean and how does it impact your pension income?

In short this means if your pension fund exceeds £1,073.100 when you either crystallise your pension or turn 75 years of age, you will be liable to pay the additional LTA tax. This will be applied differently depending on how you decide to draw upon your pension. If you take your pension as a lump sum you will be charged 55% on the amount over the LTA. If you wish to draw an income you will be charged 25% plus your nominal rate of income tax.

Will you be liable to pay the Lifetime Allowance tax charge?

Whilst a pension fund of over £1,073.100 may sound like a significant amount, it is very common for schemes to exceed this value. Many of our clients contributed a great deal to their UK pensions, as it was a way to reduce income taxes on salary and bonuses. Even if you are no longer contributing to your scheme, the growth alone could still take your UK pension over the allowance. For example if you currently have a pension fund valued around £550,000 and you average a return of 7% per annum, after 10 years you would have doubled your pension fund and now have £1,100.000.

The above table illustrates just how quickly your pension fund can exceed the lifetime allowance, should it be invested and managed correctly. If your pension is not currently invested we strongly recommend that you speak with your scheme or contact us. If you are 40 years of age today, you can also see even with a modest pension value of £100,000 you could still potentially exceed the current LTA and have to pay additional taxes on £77,515. If you were to take this as a lump sum that would equate to a tax charge of £42,633.25.

So what can you do to mitigate the Lifetime Allowance tax on your UK pension?

Some UK pension structures allow you to crystallise your pension prior to drawdown such as utilising a QROPS structure. However, there are many things to take in to account considering such as where you are resident. For example, if you currently reside in Switzerland a QROPS would maybe not be your first choice as a 25% tax charge would be levied. Although dependant on your pension value and your age a QROPS could still be beneficial. However, if you live in the EU, a QROPS is a very attractive option for most UK pension members to reduce their liabilities and maximise their future income.

Like with any other form of investment or tax advice, planning ahead and seeking professional help is a critical first step. At SuisseRock Advisory Services we have over a combined 30 years of experience helping our clients with such matters. We offer a complimentary UK pension review service and will provide you with all of the available options for you to consider.

Book your complimentary UK pension review